Build at the Back. Let the Front Pay the Debt.

In Western Australia, borrowing power has become the single biggest obstacle to upgrading your home.

Most lenders assess your maximum loan capacity at roughly four times your net annual income, after factoring in:

For someone earning $70,000 per year, borrowing capacity often sits between:

👉 $200,000 – $250,000

That figure feels limiting — especially when:

A new brick home build in Perth can cost $400,000+

Knockdown-and-rebuild projects easily exceed $500,000

Construction loans are complex and heavily scrutinised

But here’s the strategic shift:

What if the 4x income rule isn’t a limitation — but a framework for a smarter move?

Instead of building bigger…

You build smarter.

Instead of demolishing your existing asset…

You optimise it.

This is the “Use a Smaller Build to Fund Bigger Growth” strategy — using a smaller, achievable investment to unlock long-term financial growth.

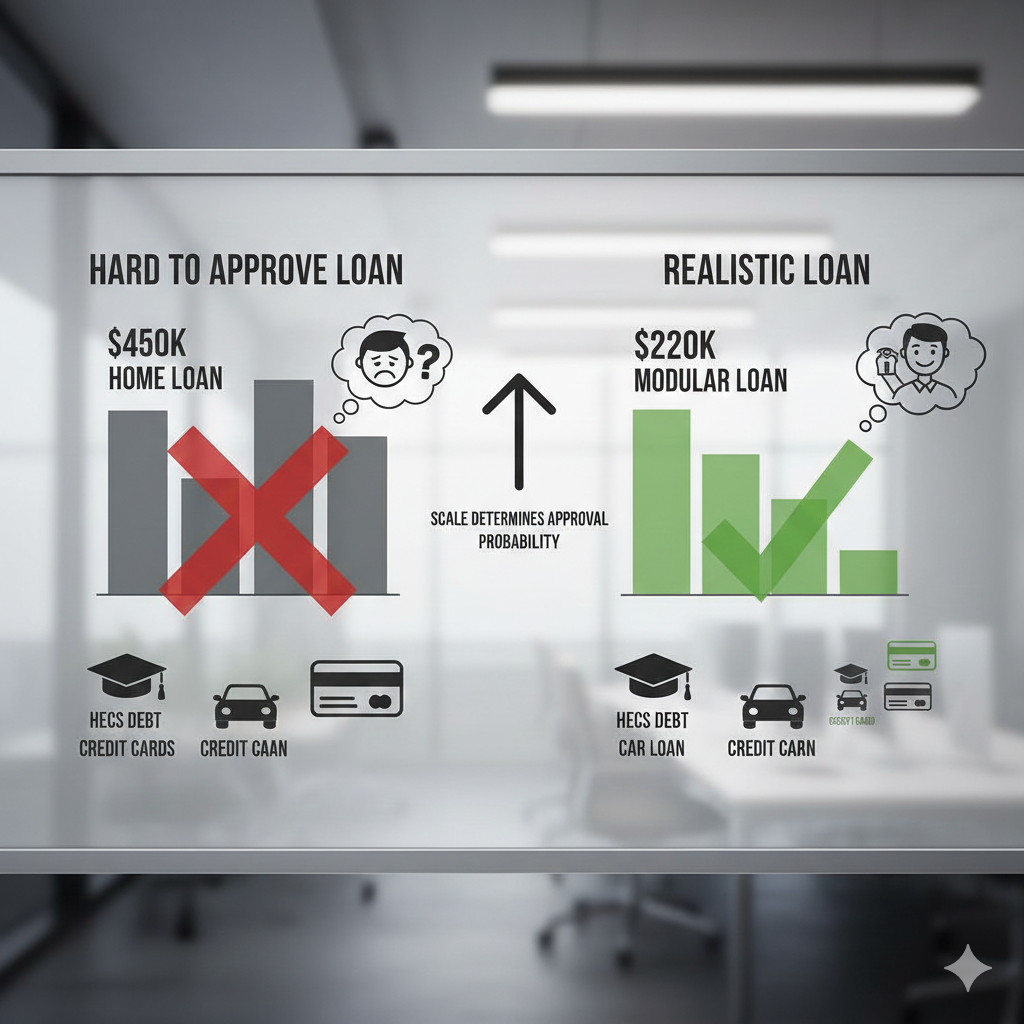

1️⃣ The Borrowing Power Reality in WA

Let’s break down the math.

A borrower earning $70,000 annually:

After tax: approximately $55,000

Monthly net income: ~$4,600

Banks stress-test your ability to repay at higher interest rates, reducing borrowing capacity.

Result:

Now compare two options:

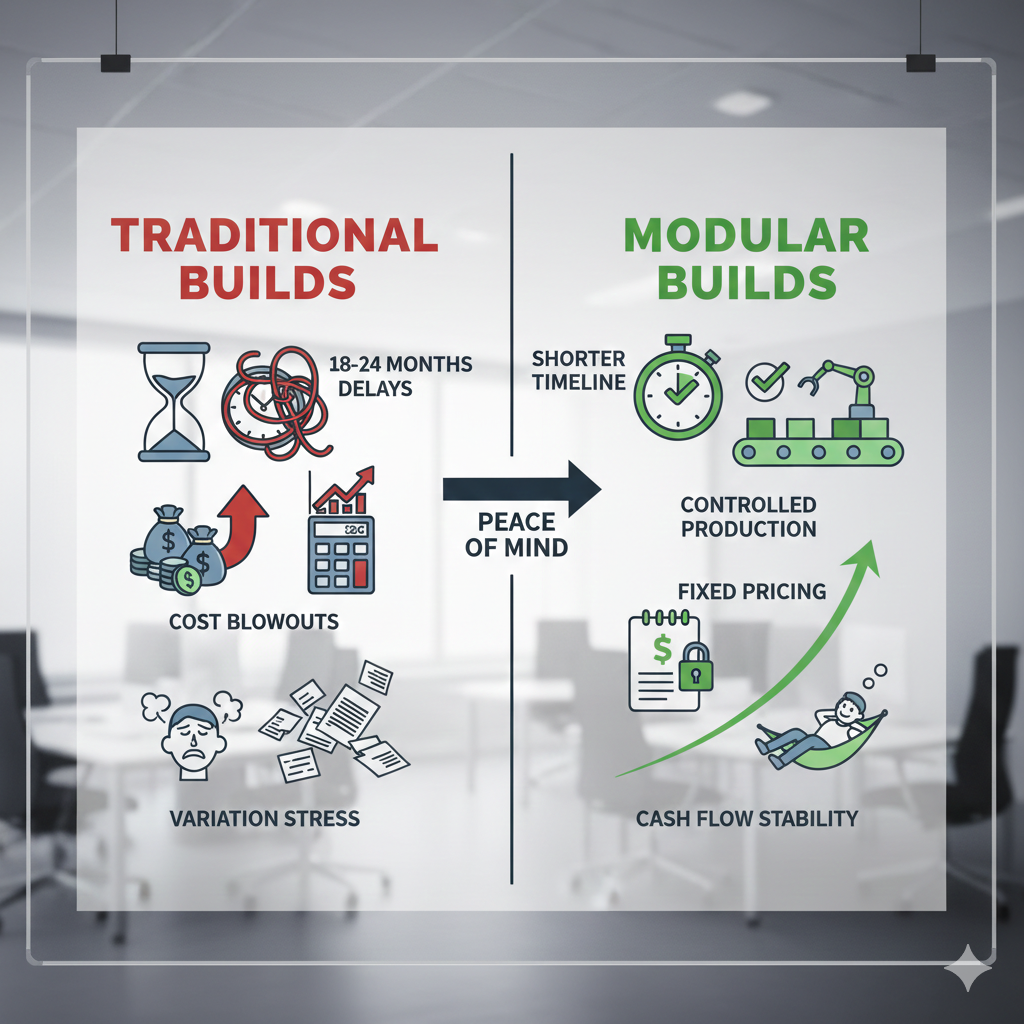

Option A: Traditional Brick Build

Estimated build cost: $400,000+

Requires large construction loan

Long build timeline (12–24 months)

High variation risk

Borrowing capacity = insufficient.

Option B: Modular Strategy

Borrowing capacity = workable.

Same income.

Different outcome.

2️⃣ Keep the Existing Asset – Multiply Its Function

The traditional mindset says:

“If I want a better house, I must demolish the old one.”

But demolition destroys:

A smarter approach is:

Instead of one income-producing asset, you now have two functional structures on a single title.

You’ve increased land utilisation without buying more land.

In high-cost environments like Perth, land is the appreciating component.

Building smarter on land you already own is leverage without acquisition risk.

“The “Swap & Pay Off” Strategy ”.